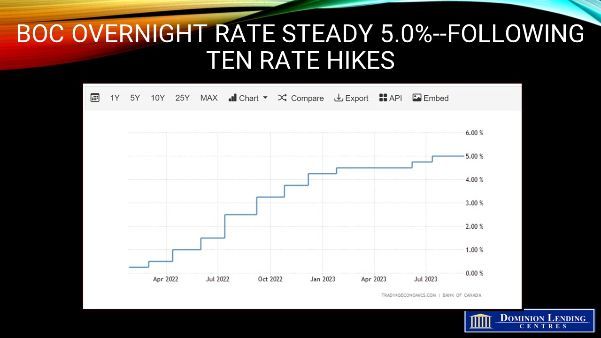

Bank of Canada Holds The Overnight Policy Rate Steady at 5%

The Bank of Canada took another breather on September 6, as was expected.

The slowdown in Q2 growth and household credit triggered the pause.

The Governing Council cautioned that they will raise rates again if inflation pressures mount.

This article is referenced from Dr. Sherry Cooper and Dominion Lending Centres

Bank of Canada Holds Rates Steady Acknowledging Economic Slowdown

With last Friday's publication of the anemic second-quarter GDP data, it was obvious that the Bank of Canada would refrain from raising rates at today's meeting.

Economic activity declined by 0.2% in Q2; the first quarter growth estimate decreased from

3.1% to

2.6%.

Today's press release announced, "The Canadian economy has entered a period of weaker growth, which is needed to relieve price pressures."

The Q2 slowdown in output reflected a "marked weakening in consumption growth and a decline in housing activity, as well as the impact of wildfires in many regions of the country. Household credit growth slowed as the impact of higher rates restrained spending among a wider range of borrowers. Final domestic demand grew by 1% in the second quarter, supported by government spending and a boost to business investment. The tightness in the labour market has continued to ease gradually. However, wage growth has remained around 4% to 5%."

Lest we get too comfy with a more dovish stance in monetary policy, the central bank warned that the Governing Council remains resolute in its commitment to restoring price stability.

Inflationary pressures remain broad-based. CPI inflation rose to 3.3% in July after falling to 2.8% in June. Much of the rise in July was caused by the statistical base effect. Nevertheless, current harbingers of inflation remain troubling. The increase in gasoline prices in August will boost inflation soon before easing again. "Year-over-year and three-month measures of core inflation are now running at about 3.5%, indicating little recent downward momentum in underlying inflation. The longer high inflation persists, the greater the risk that elevated inflation becomes entrenched, making it more difficult to restore price stability."

The Bank also continues to normalize its balance sheet by letting maturing bonds run off. This quantitative tightening keeps upward pressure on longer-term interest rates.

Tiff Macklem and company concede that excess demand is diminishing and the labour markets are easing. The unemployment rate rose to 5.5% in July, up from a cycle low of 4.9%, and job vacancies continue to decline. Net exports have slowed, and the Chinese economy has weakened sharply. Consumers are tightening their belts as the saving rate rose and household spending slowed markedly in Q1.

Monetary policy actions have a lagged effect on the economy. As mortgage renewals rise, peaking in 2026, the economic impact of higher interest rates will grow. Homeowners renewing mortgages this year are seeing roughly a doubling in interest rates.

The Governing Council will focus on the movement in excess demand, inflation expectations, wage growth and corporate price decisions.

Bottom Line

The Bank of Canada, though independent, is coming under increasing political pressure. In an unusual move, the premiers of both BC and Ontario have publicly called for a cessation of rate hikes. Even so, the BoC is keeping its hawkish bias to avoid a bond rally that could trigger another boost in the housing market, similar to what we saw last April. The government bond yield is hovering just under 5%, having breached that level recently with the release of robust US economic data.

There are two more meetings before the end of this year, and many are expecting another rate hike in one of those meetings. The odds of this are less than even, given the downward momentum in the economy.

The central bank’s next decision is due October 25, after two releases of jobs, inflation and retail data, gross domestic product numbers for July and an August estimate.

HOW TO REACH US! 📲

Call 604.398.5575 or Email us!

More Questions or READY to get started!?

Just Ask US > Click Here to set up a call or EMAIL us