FIRST TIME HOMEBUYER MYTHS | The YVR REMO Show Episode 108

We're talking today about myths and confusion related to being a first-time buyer. There are a lot of people who are not first-time buyers that will see a lot of value in this episode.

We talk a lot about investors in this market but one thing we don't talk a lot about in our podcast is people getting into the market for the first time. We get a lot of interest from people trying to figure out how to buy their first property. There are many different reasons that people are doing it and with all of the confusion and miscommunication around first-time buyer programs and what you can do, we want to set the record straight in this episode. We will highlight the most common myths and confusing points that people hear when it comes to buying your first piece of real estate. Whether you are buying your first piece of real estate or maybe your second or third, there's going to be value in this conversation if you're listening in today. A lot of these myths are things that second and third-time buyers bring to our attention as well.

You need to make sure you're working with a good team that can explain everything to you in detail and if you're making the right choices. Call your broker a year before investing so they can help you plan and have an understanding of the available programs and downpayment requirements.

We've seen real estate take off in the last couple of years. We've seen trends that people either want to get into the market as quickly as they can or they're backing out and saying I'm going to hold off. We'll talk a little bit about what that could look like and market trends. That's a valuable conversation to have when it comes to myths around real estate and where that goes.

DOWNPAYMENT MYTHS

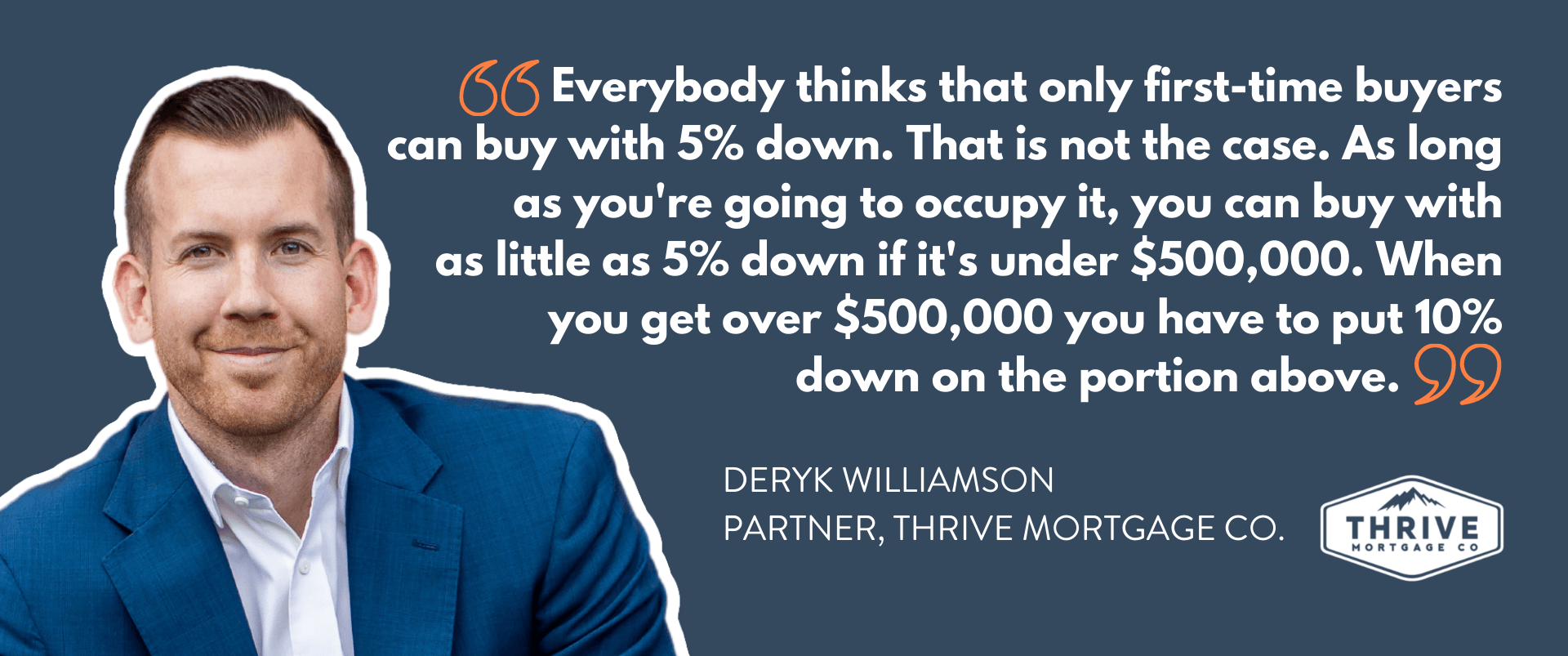

Everybody thinks that only first-time buyers can buy with 5% down. And that is not the case. As long as you're going to occupy it, you can buy with as little as 5% down if it's under 500,000. When you get over $500,000 you have to put 10% down on the portion above.

A lot of first-time buyers think that they cannot buy an investment property. We live in a market where some people have been priced out locally and they can't qualify or afford to buy something in the Greater Vancouver Fraser Valley area. That doesn't mean you shouldn't buy real estate. We've had a ton of clients that we've helped buy investment properties out of a town.

Common confusion on downpayment amounts above $500,000 that we hear is that you need to put down 10% flat. It's not 10% flat, it's just 10% on the difference.

Example:

$600,000 purchase price

First $500,000 at 5% = $25,000

$100,000 at 10% = $10,000

Anything above a million is required to put 20% down. That's a big shocker because single-family homes are hard to find for under a million dollars these days. A $999,000 purchase price is going to have $75,000 down and then as soon as you go above a million you're looking at $200,000.

A lot of people think that the 20% rule might not apply to them because they're first-time buyers. 20% is minimum on properties with a price tag of more than one million.

BUYING MULTIPLE PROPERTIES AT 5% DOWN

Can you only buy one property at 5% down? You can buy a second home with less than 20% down, you just have to qualify under the insurance guidelines. It could be for a family member or for you to move into.

A lot of our clients take advantage of something we'd like to call house hacking. There are a variety of different ways to do it with the easiest being moving into the property, living in it for a year, and then converting it into a rental. After that process, you buy another home with the minimum downpayment.

CAN YOU BUY AN INVESTMENT PROPERTY AS YOUR FIRST HOME

Real-Life Scenario

We pre-approved a client about a year ago. He was qualified for about $400,000. He came to terms with the fact that whatever he could get locally didn't make sense for him and his family. It just wouldn't work for him to be in a one-bedroom condo. He didn't have the extra income and he didn't have someone who could co-sign. Rather than him throwing in the towel and not buying anything at all, we ran some numbers and he made a goal of saving up 20%. He started working with out-of-town real estate agents, specifically in Vernon, and he watched that market. He saved and he continued to rent locally. As soon as he had his 20% down in closing costs, he pulled the trigger and bought a detached home. He paid about $450,000 for a place and it's bringing in good rent. That property has gone up in value by about $150,000 in the last eight months. He's done some renovations and he's got a good tenant in there. A lot of people might not have those conversations with their brokers. This guy could be sitting here today with the same amount of money in the bank and no real estate to help get ahead. If you find yourself in a position where buying locally doesn't make sense or doesn't work for you, remember this situation.

- A lot of people come with a minimum downpayment and it's tough to make that work even at the $450,000 mark. We've also had a client buy a second home in Powell River and rents in Langley, BC. He qualified to carry his rent and the new home that he purchased as a vacation home. That individual has put the property as an Airbnb while he's not there. That's another way to get your foot into a rental space. It's not a long-term rental, but it's a way to get into the market with minimum down.

IF YOU HAVE A COSIGNER, DO YOU STILL QUALIFY FOR FIRST-TIME HOMEBUYER PROGRAMS?

Yes, you can cosign with someone on your first home and not move into it. I've got a brother-sister duo, and the sister is looking to move in with her partner. The brother is going to come on from an income standpoint. He's going to support the qualification and help move in. They're both technically first-time buyers but he doesn't need to live on the property. She can live on the property because she's on the application. They can have a co-ownership agreement. They can also design the agreement so that he's a 50% owner in the property whether or not he's living there. Technically, it still isn't an investment for him but at the end of the day, you still qualify under the guidelines of CMHC because one of the owners is occupying the property.

What if you're a first-time buyer and your parents have bought and owned multiple pieces of real estate? If they co-sign on the property, can you qualify under any of the first-time buyer programs such as the RRSP exemption or the property transfer tax exemption? The answer to that question is yes, you can still qualify to use a percentage of that program for yourself. In the case of the homebuyers plan, like the RRSP program, you can use the entire thing under your situation.

THINGS TO KNOW

Requirements if you're a first-time homebuyer buying an investment property:

1. You can't buy an investment property with 5% down. If you're buying an investment property, you have to have 20% down but you can still do that as a first-time buyer.

2. The property transfer tax exemption, you can't use these programs if you're not going to occupy the property.

3. If you're buying a $400,000 home as an investment property, you typically wouldn't have to pay any property transfer tax. If you're going to live there, you are going to get hit with that bill.

Keep in mind these first-time homebuyer programs and exemptions are not going to work for you if you're buying for investment. That minimum downpayment is 20% for a first-time buyer or not.

FIRST-TIME HOMEBUYER PROGRAMS

First-time homebuyer programs are often misunderstood. Let's break them down.

Federal Government Homebuyer's Plan

This one is in relation to the RRSP program. Everyone thinks that you can only be a first-time homebuyer to use this program. The program allows you to dip into your RRSPs. If you take money out of your RRSPs, you have to pay tax on it unless you're a certain age. You could be 20 years old and you could have money in your RRSP. In that situation, you could take money out tax-free. You don't get taxed on that up to $35,000. You are required to pay it back over 15 years. It's a long time to pay that back, which is a nice incentive. A lot of companies paint a picture that you have to be a first-time buyer already to do that. That's not true. You could have not owned a home for over four calendar years, you could also be recently divorced or separated, a person with a disability, or supporting a person with a disability. You could use this program more than once depending on your circumstance. If you are a first-time buyer, it's just important to note that this is one of the great ways to get money out of your savings. You could be buying with another person, and still access this program for a downpayment.

With the thresholds that you can access, up to $35,000, two buyers can combine that so you're grabbing up to $70,000. You can't exceed that amount and you can't put three people together.

BC Property Tax Exemption

This one is for first-time buyers buying a home that they're occupying. In British Columbia, there are some rules and restrictions around that.

The first one is the threshold. If you're buying a property, you have to be occupying it and it needs to be under $500,000 to get the full exemption which is up to an $8,000 property transfer tax exemption. Once you go above $500,000 there is something called a sliding scale, which means for every percentage above this scale, they reduce the rebate. For $525,000 you have to now pay the entire amount at $500,000. There's a full exemption, so there's a percentage that you still have to pay. You have to occupy the property, you have to file taxes the previous year in British Columbia, or lived there for 12 months. Double-check with your lawyer on your qualifications and whether or not you're qualified. We've seen before where people tried to qualify for exemption and didn't live in British Columbia for that period. They need to then be Canadian for the most part or permanent residents to qualify for this. It's got to be owner-occupied. You can't be a foreign resident and take advantage of this program.

If you're on the fringe of buying something that $550,000 and can find something a little bit cheaper to save, it's beneficial. We've also had a lot of clients see it make sense to spend the extra money on transfer tax because you get a two-bedroom. That two-bedroom is going to appreciate more than one bedroom and it's going to be a longer plan for you.

Don't build your desired home around saving money.

With brand new pre-sales, you're buying directly from the developer and no one's lived there before. If it's owner-occupied and under $750,000 you do not pay transfer tax above that $750,000. You do not need to be a first-time buyer for that. As long as it's owner-occupied under $750,000 you do not pay a transfer tax.

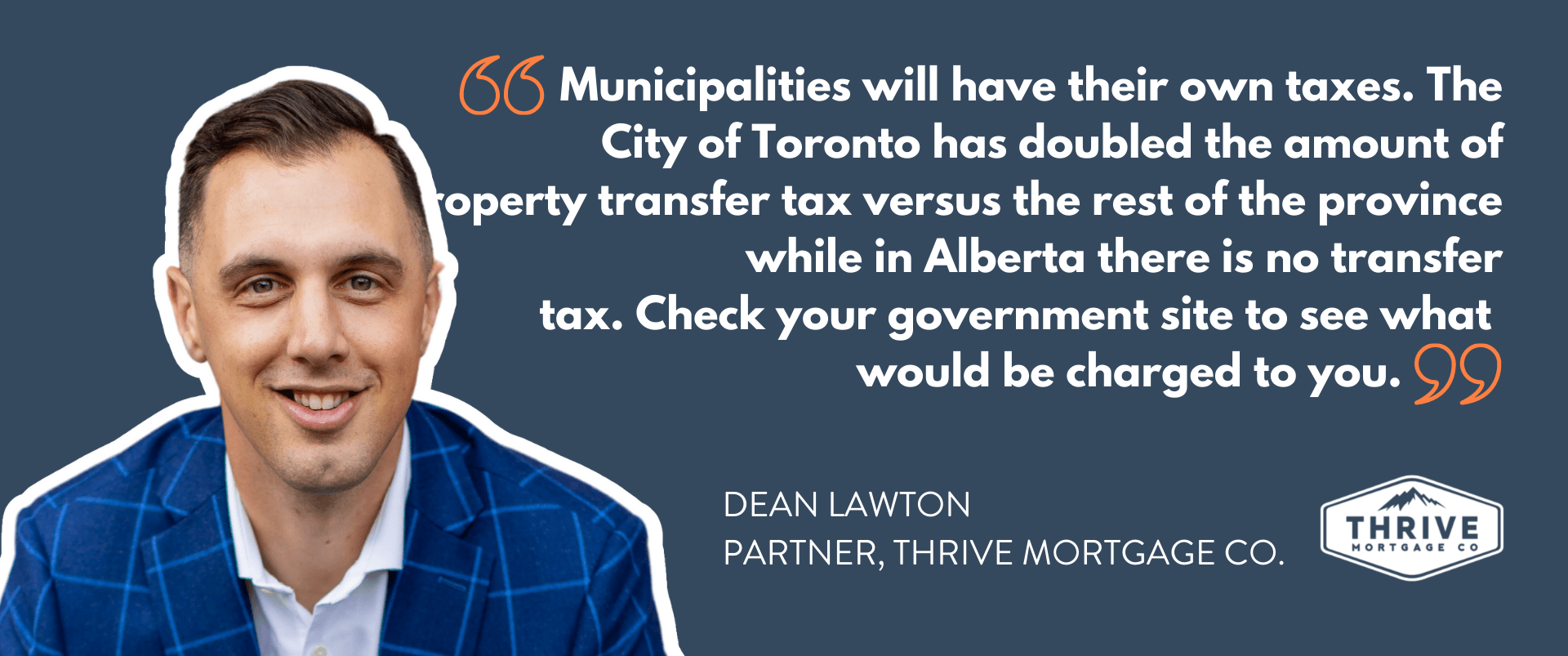

Municipalities will have their own taxes in some cases. The City of Toronto has doubled the amount of property transfer tax versus the rest of the province. In Alberta, there is no transfer tax. Check your government site to see what would be charged to you.

MYTHS SURROUNDING BUYING & CLOSING COSTS

There are a lot of myths around the closing cost.

What are closing costs?

What would you have to pay?

Can you roll that into the mortgage?

If you are purchasing a property and putting 5% down, technically you don't roll the additional costs into the mortgage. These can be legal fees and expenses. Some lenders can qualify you for cash back programs. They lump an extra amount of money back to you at the lawyer's office to cover some of the closing costs. There are some rules, restrictions, and costs around that. If you break that early in the next five years, not only will you pay a relatively large penalty, but you'll also have to pay back the entire cash back amount as well.

You can roll closing the costs with some lenders if you qualify but it is more of a cash-back program. What if you have a $60,000 truck and you want to add that to your mortgage? Technically speaking you can't because most of these cash back programs don't qualify for that kind of money. We're talking about 1% to 3% of the balance of the loan. If you're borrowing $500,000 that is $15,000. It's meant more of like a small amount to help someone get across the line or consolidate. There's some creativity that can be had there.

Closing costs that you can expect to pay to go into this if you're a first-time buyer are transfer tax and municipality-dependent property transfer tax. If you're over the threshold, there are also legal fees. We tell people it's around $1,600. A lawyer provides an exact quote. Outside of that, if you're buying with 20% down there could be an appraisal. If you choose to do an inspection on a home, they're usually about $750,000 depending on the size and scope. Sometimes there's a requirement to pay off a debt to allow you to qualify for that mortgage.

What isn't a closing cost? If we tell you that you have to pay your credit card to zero before completion, that's not necessarily a closing cost.

Those are the items that you want to prepare for going into a purchase and transfer tax in BC. Budgeting will help because it can be very dramatic, especially with current house prices.

How Can Thrive Help You?

We have a very helpful budgeting tool as part of our software when we pre-approve our clients. It summarizes all these numbers for you, which can be very helpful. Click our mortgage calculator below!

HOME INSPECTIONS

One thing that's talked about a lot is the home inspection. It is not a requirement of the lender and the bank will not make you do a home inspection. It is your choice, but it's highly recommended. There are experienced individuals that can assist you with this

If you have experience as a home builder, you should be okay. You should know what you're looking for but we've seen that work against people as well. We've seen a situation where an uncle has renovated a couples home and it ended up costing them $50,000 within two months. This happened because they didn't catch some of the potential issues.

MYTHS AROUND CREDIT SCORES

People don't reach out to start the process early enough. They don't reach out to start the conversation. We're finding that people don't have enough credit quite frequently. It's not just the credit score, but creditworthiness. What we mean by that is it's one thing to have a cell phone in your name and to pay everything by cash, which a lot of people tend to do. It's another thing to prove that you can pay back your credit via multiple accounts such as a credit card or a line of credit. We're not recommending someone go out and take on a bunch of debt.

We're noticing people have low credit for two reasons:

- They don't take care of their credit and they're not paying it off on time.

- They don't have enough credit and it's limiting their qualification. The easy way around that is to make sure you have two credit lines and just use them monthly on gas, groceries, or other low-cost necessities.

It's not just a credit score, it's a very detailed report. The banks are looking through that report and reading it. The score is one small item on a report that could be four pages long. There is a lot of very detailed information that we're going to be looking at, not just miss payment and score.

How much of a limit does your credit card have? A $500 credit card limit is not going to be enough if that's your only product. We've seen many people have a $500 credit card that they got when they were 19 and you fast forward that's all that they have. You can call the bank and ask to increase that limit. It's typically done over the phone, or in most cases, they're already pre-approved you for that and it's just a click of a button on their online banking. Those little adjustments could help you.

You need to use your credit to get credit to get good credit. We have seen applications get declined with a good credit score. The bank comes back and says it's too thin. That's the word that they use, the credit is too thin and there's not enough here to justify good credit.

There are a lot of things that are going to vary on credit reports that a broker or bank pulls versus your credit report. The score is one of them. Those scores will differentiate, so don't be alarmed when your score is different. There are a lot of times we'll notice accounts that you thought you closed and are still showing as an active account on the report. Some of these issues that come up on credit reports literally can take up to six months to rectify. This again, is why preparation and starting the process early is always a great idea.

GETTING A MORTGAGE AS A FIRST-TIME BUYER LEAVING YOUR EDUCATION TO BEGIN A CAREER

What if you're getting out of university and starting a new job, what does that look like? We have seen a variety of age groups that don't have a strong working history with full-time hours. If you went to school and you're working in your trade of choice at full-time and guaranteed hours, lenders will consider your income.

We hear this quite frequently where people don't buy because they walked into their bank and are told they can't get a mortgage because they need to have a year under their new position. We've got tons of lenders who will consider your qualification, it just has to be a good story.

It's all about the story.

The other thing to note is that a lot of people, the first thing they do is a Google Search on mortgage rates. They apply with an online lender and they get declined and then they don't do anything for a year. If you're going straight to a lot of the branches, you're dealing with people who are maybe not qualified and they're just basically looking at guidelines. If you're going online, it's the same thing. That's why they offer certain products and rates at a lower cost. It's because they're piling in the easy stuff quickly. If you're a first-time buyer and you think you have a unique scenario, you should talk to a professional.

WHAT HAPPENS IF I FINANCE A NEW VEHICLE BEFORE I QUALIFY FOR A MORTGAGE?

Don't take on a car loan before you buy your house. Do whatever you need to do before you get the car loan. We get people buying car loans with payments of around $1,000 to $1,200 and they can't qualify for a house. For every $400, you're losing $100,00 in mortgage qualification. Even if your car loan is only $3,000 you're probably better to pay that off.

As a first-time buyer, lenders are looking for guaranteed income if you've started in the last 12 months and you're putting down 5%. In most cases, you need a 24-month average or two-year history.

Lending programs and guidelines change monthly and weekly.

We're on Instagram!

instagram.com/thrivemortgageco

Check us out on Facebook!

How to Reach US! 📲

Call 604.398.5575 or Email us!

More Questions or READY to get started!?

Just Ask US > Click Here to set up a call or EMAIL us